A comprehensive intake form that collects client debt details, creditor information, income sources, expenses, and repayment capacity before your first consultation.

Financial planners and debt management advisors who need complete financial pictures of clients struggling with multiple debts, late payments, or unclear repayment strategies.

Send it 48-72 hours before initial consultations so clients can gather loan documents, credit card statements, and calculate their actual monthly expenses with supporting documentation.

A client walks into your office with credit card statements, loan documents, and a spiral notebook full of scattered numbers. You spend the first 30 minutes just figuring out what they owe and to whom. Sound familiar? Incomplete information doesn't just waste time - it delays the debt relief your clients desperately need.

A debt management questionnaire solves this problem. It captures everything upfront: creditor details, interest rates, income sources, payment history, and financial goals. You get organized data before the first meeting. This post covers what the form includes, how to use it effectively with clients, and a free template you can customize. Let's break it down.

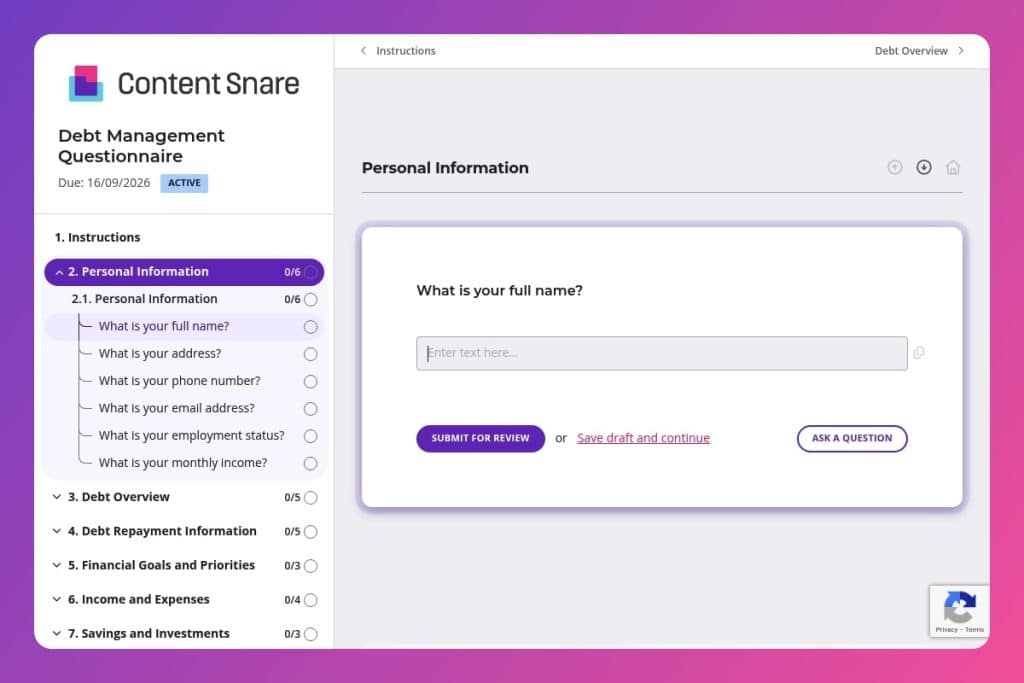

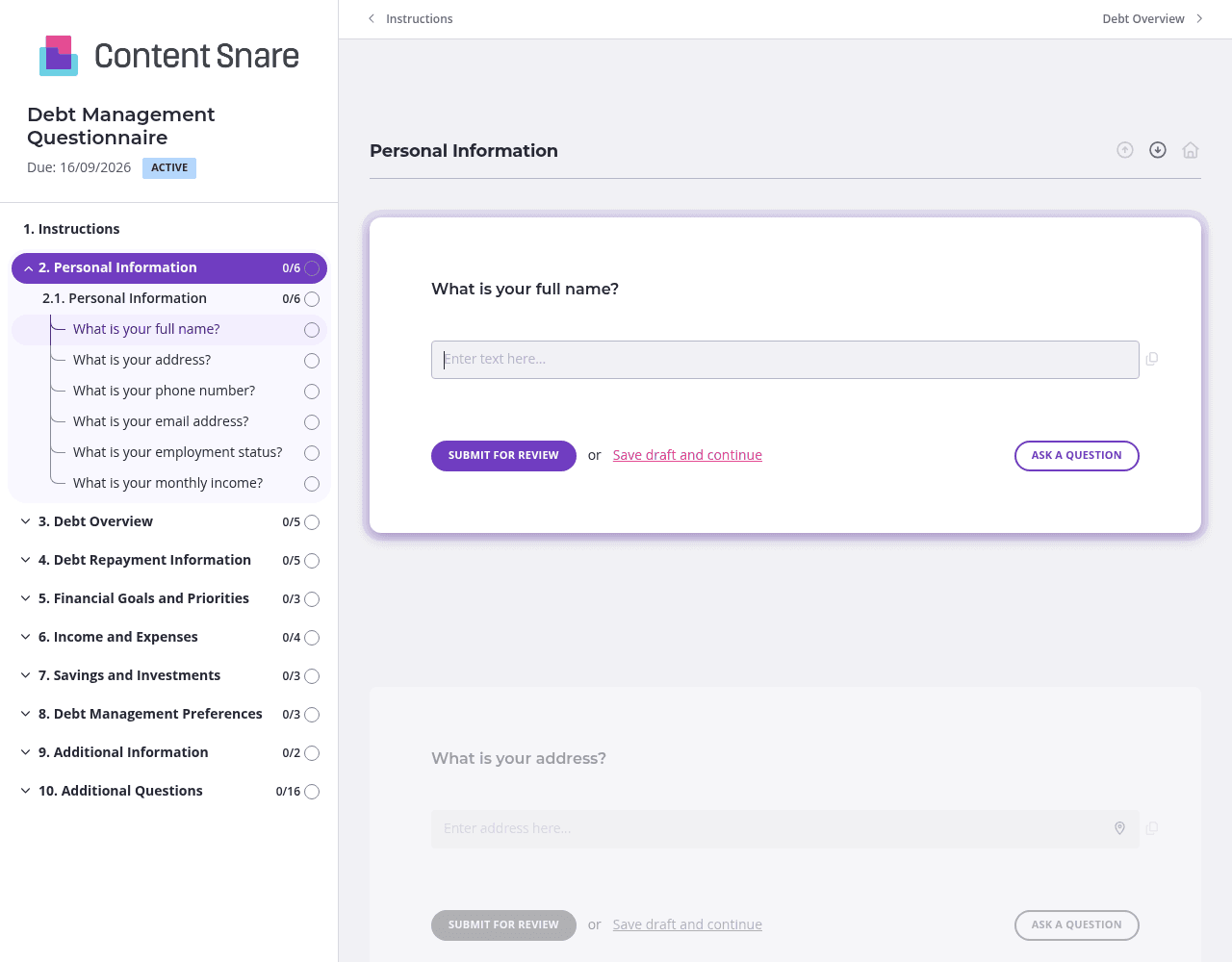

Personal Information

Use this block to capture identifiers and income context for verification and baseline capacity assessment.

Debt Overview

Establish the scope, composition, and pricing of liabilities to guide prioritization and negotiation strategy.

Debt Repayment Information

Document current repayment terms, compliance, and potential shocks to assess feasibility and risk.

Financial Goals and Priorities

Clarify desired outcomes and trade-offs so the plan aligns with client intent and behavioral fit.

Income and Expenses

Build an accurate cash flow to size affordable payments and identify levers for adjustment.

Savings and Investments

Understand buffers and protected assets to avoid liquidity risk and preserve long-term capital.

Debt Management Preferences

Capture prior program experience and preferred approaches to improve adherence and fit.

Additional Information

Leave space for nuances, constraints, or risk factors not covered above.

Send the form before the initial consultation: Give clients 48-72 hours to gather documents like credit card statements, loan agreements, and pay stubs. They'll provide more accurate creditor information and interest rates when they're not rushing through it in your waiting room.

Flag the debt prioritization question for deeper conversation: When clients indicate which debts they prioritize and why, that's gold. Use their answer as a starting point in your meeting to understand emotional factors - maybe they're prioritizing a family loan over a high-interest credit card. These insights shape realistic repayment plans.

Cross-reference income against expenses and debt payments: Before your meeting, calculate their debt-to-income ratio and check if their stated monthly expenses leave room for their claimed debt repayments. Discrepancies aren't lies - they're opportunities to help clients see where money actually goes.

Use the bankruptcy and payment history questions as early warning signals: If someone's behind on payments or has filed bankruptcy previously, you'll need specialized strategies from day one. Knowing this upfront lets you prepare appropriate solutions instead of pivoting mid-consultation.

Create a summary sheet from their responses: Pull key numbers - total debt, monthly income, current payments, and available cash flow - into a one-page overview. Share it with clients at the start of your meeting so everyone's looking at the same picture. It turns abstract anxiety into a concrete plan.

Debt discussions overwhelm clients quickly. Content Snare lets you split your questionnaire into logical pages - Personal Information, Debt Overview, Income & Expenses, Financial Goals. Clients tackle one section at a time instead of facing a 40-question avalanche. They can save progress and return later, which matters when someone needs to dig through filing cabinets for creditor statements or calculate household expenses.

The "types of debt" and "creditor information" questions trip people up. Someone might list "credit cards" but forget to include the specific bank names, account numbers, and balances you actually need. Content Snare lets you add instruction text directly below each question. Spell out exactly what you're looking for: "List each credit card separately with the bank name, last 4 digits, current balance, interest rate, and minimum payment." You'll get complete information the first time instead of playing email tag for missing details.

Clients mean well, but they procrastinate on financial paperwork. Content Snare sends automatic reminder emails on your behalf so you don't have to chase anyone down. The reminders come from your branded email address, keeping the relationship professional. You'll know exactly who hasn't completed their questionnaire and who's ready for their consultation - all from your dashboard.

Email threads lose attachments. Google Forms can't handle sensitive financial data securely. PDFs come back half-completed or illegible. Content Snare gives you a professional, secure system designed specifically for collecting detailed client information - with automatic reminders, progress tracking, and ISO 27001 certification to protect your clients' financial details.

Financial advisors and planners trust Content Snare because it handles complexity without overwhelming clients. Thousands of businesses worldwide use it to streamline their intake processes, and it has hundreds of 5-star reviews across G2, Capterra, and Trustpilot.

The debt management questionnaire is just one application. Financial planners also use Content Snare for:

Content Snare integrates with the tools you already use - your CRM, project management software, and cloud storage - so client data flows directly into your workflow without manual data entry.