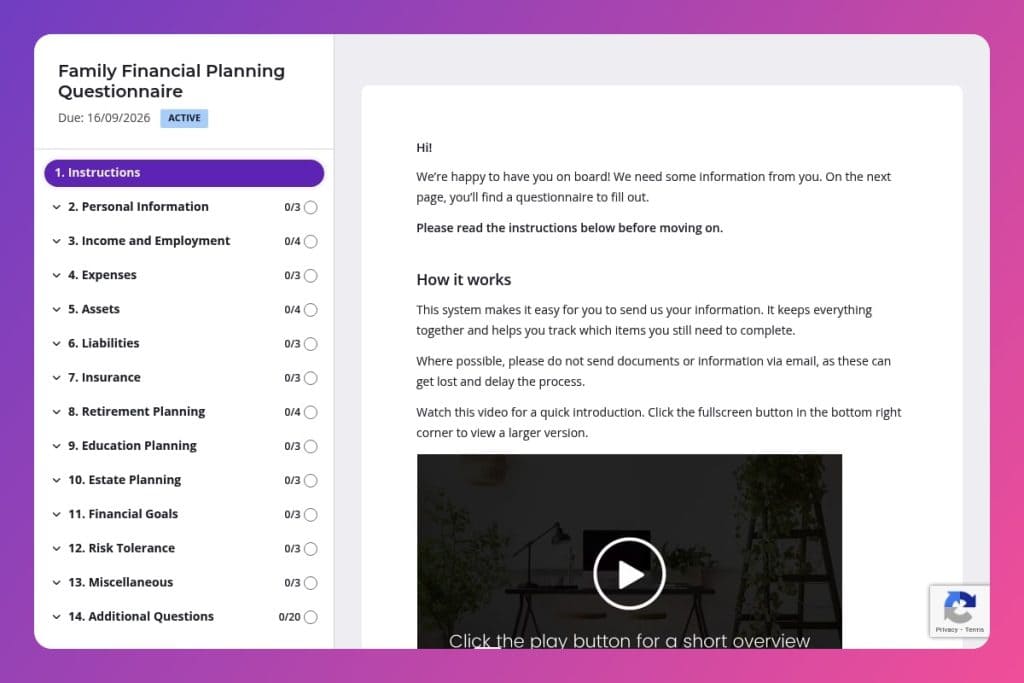

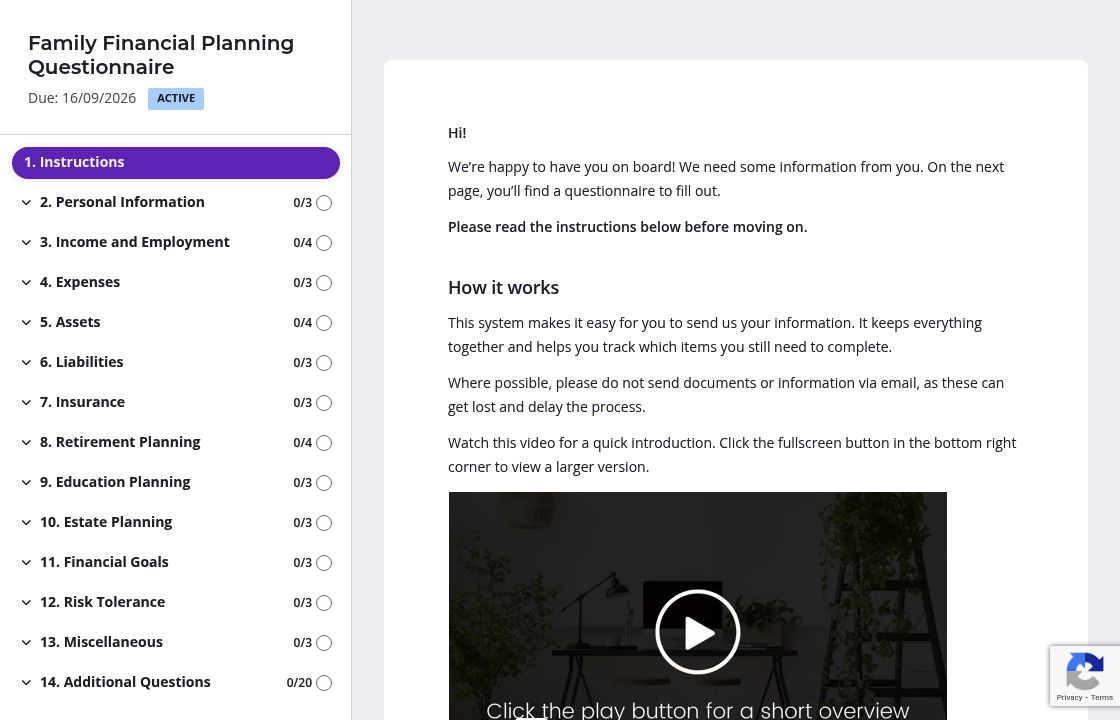

A comprehensive intake form that collects detailed financial information including household income, assets, liabilities, retirement accounts, insurance coverage, and estate planning status before client meetings.

Financial planners and wealth advisors who need to gather complete client financial data upfront to prepare tailored financial plans and eliminate scattered discovery conversations.

Send this questionnaire 48 hours before initial client consultations to give families time to gather documentation and provide accurate financial details for your first meeting.

You're juggling too much information during client discovery - scattered notes, forgotten details about dependents, vague answers about retirement accounts. The result? Multiple follow-up calls, delayed plans, and frustrated families who expected clarity from the first meeting.

A family financial planning questionnaire solves this. It captures everything upfront - household income, liabilities, retirement goals, insurance coverage, and estate planning status - so you walk into meetings prepared. This post covers what the form includes, how to use it effectively with clients, and where to grab a free template. Let's break it down.

Personal Information

Collect baseline household data to contextualize goals, obligations, and planning assumptions.

Income and Employment

Establish current and near-term earning capacity to drive cash-flow planning and tax strategy.

Expenses

Map ongoing and upcoming outflows to build an accurate cash-flow and reserve model.

Assets

Inventory assets to assess liquidity, diversification, and collateral options.

Liabilities

Detail liabilities to evaluate debt service, refinancing opportunities, and risk exposure.

Insurance

Confirm current risk transfer arrangements and potential coverage gaps.

Retirement Planning

Quantify retirement readiness and plan design across qualified and nonqualified sources.

Education Planning

Clarify timelines and targets for education funding and vehicle selection.

Estate Planning

Surface existing documents and directives to align titling, beneficiary designations, and transfer intent.

Financial Goals

Prioritize objectives to anchor the plan and allocate resources.

Risk Tolerance

Calibrate portfolio design to client risk capacity, tolerance, and experience.

Miscellaneous

Capture service expectations and open issues to shape engagement cadence.

Send it before the first meeting: Give clients at least 48 hours to complete the questionnaire before your initial consultation. They'll need time to gather documents - mortgage statements, retirement account balances, insurance policies. You'll get more accurate data and fewer "I'll have to check on that" moments during your meeting.

Flag high-priority sections upfront: Not every client needs to answer every question in detail right away. If someone's primary concern is retirement planning, tell them to focus on the retirement, income, and assets sections first. You can circle back to estate planning or education funding once the immediate priorities are addressed.

Use responses to build your meeting agenda: Review their answers on financial goals, risk tolerance, and specific concerns before you meet. Structure your conversation around what matters most to them - whether that's eliminating credit card debt, funding a 529 plan, or adjusting their investment strategy. They'll feel heard, and you'll stay on track.

Cross-reference liabilities with goals: When a client lists aggressive financial milestones but also shows significant outstanding loans or credit card debt, that's your cue. Use the questionnaire data to have a realistic conversation about debt management before pursuing new investments or major purchases.

Schedule a follow-up review cadence based on their answer: The miscellaneous section asks how often they want to review their plan. Honor that preference and set expectations immediately - whether it's quarterly check-ins or annual updates. It shows you're paying attention and helps you stay proactive with client relationships.

This questionnaire covers a lot of ground - assets, liabilities, retirement accounts, insurance policies, estate planning. That's overwhelming in one long scroll. Use pages to separate major topic areas: one for income and expenses, another for assets and liabilities, a third for retirement and education planning. Clients can tackle one section at a time without feeling buried. They're more likely to complete it, and less likely to skip questions because they got fatigued halfway through.

Financial planning questionnaires require clients to dig up documentation - W-2s, mortgage statements, 401(k) balances, insurance policy details. People get busy and forget. Automatic reminders keep your form top of mind without you having to send "just checking in" emails. You stay professional, clients stay on track, and you get the information you need to move forward.

Not every family needs to answer every question. A couple without kids doesn't need the education planning section. Someone who rents doesn't need questions about property value or mortgages. Conditional logic hides irrelevant questions based on earlier answers - like skipping estate planning details if they haven't established a will yet. The form feels personalized, and clients don't waste time on sections that don't apply to them.

Questions about "total household income" or "estimated value of your primary residence" can be interpreted different ways. Add brief instructions or examples directly in the form: "Include salary, bonuses, and commissions before taxes" or "Use your most recent property tax assessment or online estimate." Clients get it right the first time, and you avoid follow-up clarifications that delay the planning process.

Email attachments get lost. Shared documents create version chaos. Phone calls mean manual note-taking and missed details. Content Snare centralizes everything - clients answer once, you get organized responses, and nothing falls through the cracks.

You're also working with sensitive financial data. Content Snare is ISO 27001 certified and trusted by financial planners and thousands of businesses worldwide to handle confidential client information securely.

The platform has hundreds of 5-star reviews across G2, Capterra, and Trustpilot. It integrates with the tools you already use, so client data flows directly into your CRM or practice management software without manual data entry.

This family financial planning questionnaire is just the starting point. You can use Content Snare to collect:

Every form stays organized, every client stays on track, and you spend less time chasing information.