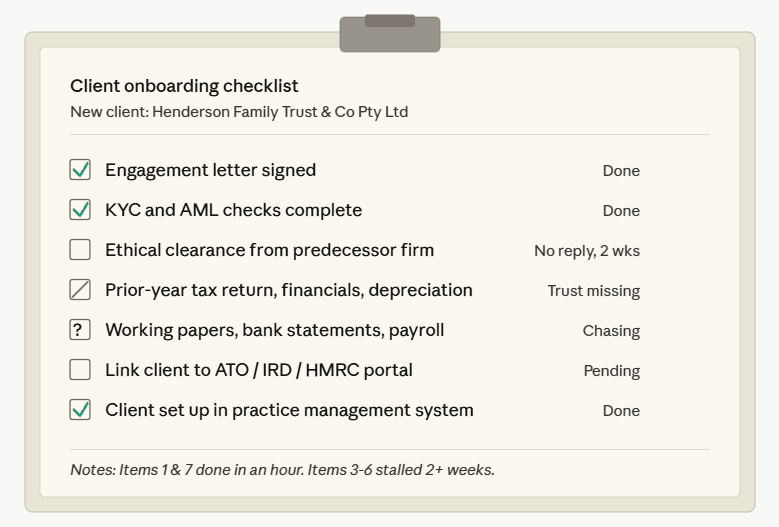

You've sent the engagement letter. The client signed it. Two weeks later, you're still missing the prior-year tax return, the closing trial balance for one of three entities, and an answer on whether the spouse is a beneficiary of the trust. The work hasn't started and the deadline hasn't moved.

That gap, the one between "they signed" and "we have what we need," is where most accounting firms lose the first few weeks of every new engagement. It's an information collection problem that gets worse as a firm scales. Our guide covers what accounting client onboarding looks like for a modern practice, where the time actually goes, and what to do about the step that breaks most often.

What accounting client onboarding actually means

Client onboarding is the process of moving a new client from signed engagement to first deliverable. For an accounting firm, that means doing all of this in sequence:

- Send and execute the engagement letter

- Run KYC and AML checks

- Contact the predecessor firm for ethical clearance

- Collect prior-year tax returns, financial statements, depreciation schedules, and the closing trial balance

- Gather current-year working papers, bank statements, payroll data, and entity documents

- Link the client to your tax agent or accountant portal (ATO, IRD, HMRC, depending on jurisdiction)

- Set up the client in your practice management system

In practice, items one and seven take a few hours each. Items three through six can take six weeks, two emails per week, and most of your project manager's patience.

Where accounting practices lose time

The middle of that list is where engagements stall, and the same two patterns show up again and again. One comes from Content Snare’s sales calls and customer interviews. The other is loud on Reddit, in threads where accountants vent about a problem the vendor pitches rarely acknowledge.

1. The information loop

The pattern isn't one slow client. It's the entire onboarding-and-collection step, and it's near-universal. Sarah Bettridge of Ex Animo Advisory put it this way in our customer interview:

“I've spent so much time at large accounting firms. We've done brainstorming sessions with hundreds of people about what our worst thing is. And it is onboarding and collecting information from clients."

2. Client portal refusal

One CPA on Reddit summed it up after another round of chasing: "They'll respond to an email instantaneously, but will schedule 4 days out to login to the portal for the first time and password set-up."

So, the portal exists, but the client won't use it. That’s why the firm reverts to email, while the audit trail disappears.

Pro tip: The fix that actually moves the number is removing both friction points at once, with one tool clients will actually use. Across the customer base, firms using Content Snare report a 71% reduction in time spent chasing clients for information, with the median firm dropping from 25 hours a month to 5. That time goes back into billable work or capacity to take on the next engagement. We unpack how below. |

The three things that make accounting onboarding work

Most onboarding advice focuses on the workflow design. That part is solved: the steps haven't changed in twenty years. What matters is whether each step actually happens on time, the same way, every time. Three things determine that.

Client experience

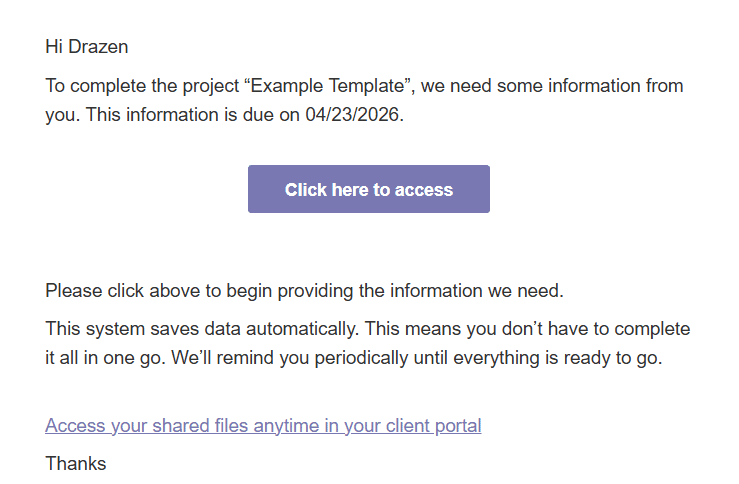

If the client has to remember a password to send you their tax docs, the docs arrive late (and the lodgment date doesn't care). Content Snare uses link-based access, so clients click the email and land on their request:

No login, account creation, or password resets. Every keystroke auto-saves, so a client filling out a long onboarding questionnaire on the train can close the browser, come back at 11pm, and pick up exactly where they left off.

This is the difference between "I'll do that this weekend" actually happening and not.

Security and trust

Accounting onboarding involves sensitive material that doesn't belong in email:

- Tax file numbers, IRD numbers, National Insurance numbers

- Passport scans and other government-issued ID

- Bank statements and loan documents

- Proof of address and source of funds documentation

Content Snare is ISO 27001 certified, which means it follows strict security practices to keep your data secure. The system uses military-grade encryption and applies per-company encryption keys so one firm's client data is cryptographically separated from every other firm's.

For UK firms under MLR and Australian firms under the Tranche 2 AML/CTF regime, that distinction matters during a supervisory review.

Flexibility

A firm doing tax returns, business advisory, audit, and self-managed super fund work doesn’t need four separate intake tools. It needs one tool that can run a 40-item PBC checklist for an audit, a short director's declaration for a company setup, and a tax return questionnaire for an individual, without the team having to learn three interfaces.

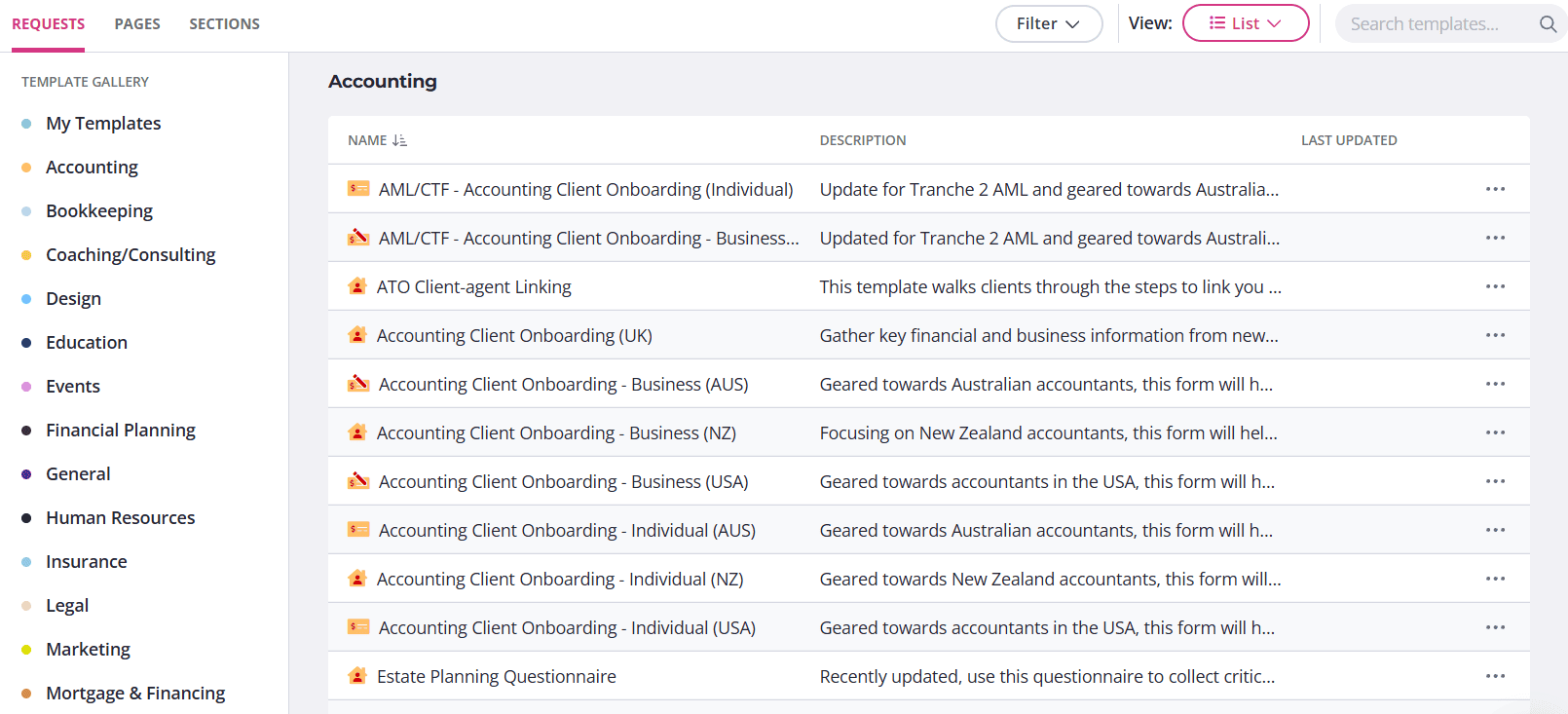

Content Snare ships with 110+ form templates covering accounting client onboarding (AUS), (UK), (NZ), tax preparation, audit, KYC, and ethical clearance for accountants. Use them as-is, edit them, or build new ones with the AI request builder.

A working onboarding checklist for accounting firms

Tooling is one half of the answer. The other half is having a defined checklist that runs the same way regardless of who in the firm is onboarding the client.

The list below is jurisdiction-aware and service-neutral, so adapt it to your mix. Whether you run it inside Content Snare, your practice management system, a shared spreadsheet, or any other system, the items themselves are what matter.

Engagement and scope:

- Engagement letter (signed)

- Scope confirmation and fee agreement

- Authority to act / agent appointment

Identity and compliance:

- Photo ID for all directors, trustees, partners (passport or driver's license)

- Proof of address (utility bill, bank statement, recent correspondence)

- Trust deed or company constitution

- KYC / AML checks completed and recorded

- For AUS firms, ATO client-agent linking

- For UK firms under MLR, source of funds documentation where applicable

Predecessor firm handover:

- Ethical clearance request sent

- Prior-year working papers received

- Outstanding queries from predecessor noted

Historical financial information:

- Prior-year tax return(s) for all entities

- Prior-year financial statements

- Depreciation schedules and fixed asset registers

- Outstanding ATO/IRD/HMRC correspondence

- Tax loss schedules and franking accounts (where relevant)

Current-year information (for tax engagements):

- Bank statements for all business accounts (full year)

- Loan statements

- Payroll summary and superannuation/KiwiSaver/PAYE reports

- Sales and purchase records, GST/VAT returns

- Investment statements (managed funds, shares, crypto)

- Rental property income and expenses

System setup:

- Client added to practice management system

- Recurring tasks scheduled

- Internal team briefed

- First check-in meeting booked

A PBC checklist template covers most of the historical-and-current sections for audit and advisory work. For tax-specific intake, the regional templates above are closer fits.

How Content Snare fits with what you already use

Content Snare is a secure client portal purpose-built for collecting documents and information from clients. Accounting firms in Australia, New Zealand, the UK, and the US use it to replace the email back-and-forth with a single structured request.

It works alongside the practice management system you already have. If you run Karbon, Xero Practice Manager, FYI, or SuiteFiles, Content Snare handles the client-facing collection step and pushes the documents and structured data back into your stack via direct integrations, Zapier, or webhooks. You don't replace anything, you just replace the email part.

For accounting firms specifically, that translates to roughly half the time spent on onboarding and significantly better data quality coming in the door. Liston Newton Advisory put it directly:

"Content Snare has increased our efficiency by 50%, but we're still continuously improving it. Data accuracy and completeness improved massively, I would say 70%."

The fastest way to find out if Content Snare works for your accounting firm is to run a real client through it.

You get 14 days, no credit card, and a library of accounting templates built for AUS, NZ, UK, and US firms.

FAQ

How long should onboarding a new accounting client take?

For a straightforward individual tax client with one entity, allow 3 to 5 business days from signed engagement to having everything you need to start work. For a business client with multiple entities, payroll, and a trust structure, plan for 2 to 4 weeks if the client is responsive. The variable is not the work, it's how quickly the client returns information.

Do clients actually use Content Snare, or do they ignore it like every other portal?

Content Snare doesn't require a login or account. Clients click the link in your email and land directly on their request, with auto-save on every keystroke so they can fill in what they have and come back to the rest. Across the customer base, 79% of firms report direct positive feedback from clients about the experience. The most common reason clients refuse other portals is friction at the login step, and Content Snare doesn't have one.

We already use a practice management tool. Do we really need another software?

Practice management systems are built to run your internal workflow. Content Snare is built for the client-facing collection step, which is the part that lives outside your firm's systems by definition. The two work together: Content Snare collects, your practice management system orchestrates. Many firms keep both because the client experience of a purpose-built collection tool is materially better than the portal that ships with practice management software.

Is Content Snare secure enough for tax documents and client ID?

Content Snare is ISO 27001 certified, uses military-grade encryption, and applies per-company encryption keys, which is the standard required by most professional indemnity insurers and supervisory bodies. For UK firms under MLR and AUS firms under Tranche 2 AML/CTF requirements, the platform supports the document handling and audit trail expectations both regimes apply.

What's the best way to handle KYC and AML checks during onboarding?

Run them upfront, before any substantive work begins, and document everything in a single place. The standard accounting practice is to verify identity with government-issued photo ID and proof of address, screen against PEP and sanctions lists, and record the date and method of verification. Doing this inside the same tool you use for the rest of your onboarding collection avoids the cross-system reconciliation problem at year-end. See the KYC onboarding guide for the full process.

What if a client never finishes their onboarding request?

Set automatic reminders on a cadence that matches the urgency of the engagement: every two days for tax-deadline work, weekly for non-urgent onboarding. Most clients respond to the second or third reminder. For the persistent non-responders, escalate to a phone call once the reminders have given you an honest answer about whether the client is engaged.