If you're an accounting firm trying to figure out AML screening, you're not alone. With new obligations on the horizon, most firms are in the same boat: they know they need to do something, but they're not sure exactly what that looks like day to day. The good news is that setting up a screening process doesn't have to be overwhelming. In this guide, we'll walk through how to build an AML screening workflow across your firm that actually works in practice.

What AML screening actually involves

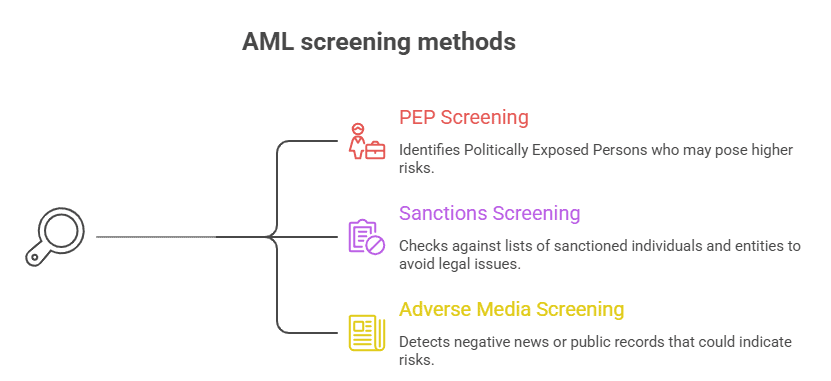

AML screening means checking your clients against various data sources to spot potential risks such as money laundering, fraud, or sanctions exposure. For accounting firms, this sits within your broader client due diligence process and it’s not a single check. It’s a combination of different types of screening, each covering a different kind of risk.

PEP and sanctions screening

Politically exposed person (PEP) checks and sanctions screening form the foundation of AML compliance. They help you identify whether a client holds a high-risk public position or appears on government watchlists. These checks are now standard practice and, in most cases, are handled through automated systems.

If you need a step-by-step breakdown of how these checks work and how to run them in practice, see our guide to PEP and sanctions screening.

Adverse media screening

Adverse media screening looks for negative news or public information about a client. This can include links to fraud, financial crime, corruption, regulatory breaches, or other concerning activity. Unlike sanctions or PEP lists, this information doesn’t sit in a single database because it comes from a wide range of sources. In other words, adverse media screening requires more judgment.

This is also where many firms fall short. A client may not appear on any official list but still have a history of issues that raise legitimate concerns. Adverse media screening helps surface those risks, particularly for:

- Clients with complex business activities

- Higher-value engagements

- Clients operating across multiple jurisdictions

Bear in mind that the goal isn’t to treat every negative mention as a red flag. On the contrary, the idea is to look for credible sources and context.

Document your findings even when no issues are identified, you should record what was checked and how you reached that conclusion. This creates a clear audit trail and demonstrates that proper due diligence was carried out and not just assumed.

The risk-based approach to AML screening

Not every client presents the same level of risk, and your screening process shouldn’t treat them as if they do. A risk-based approach means adjusting the depth of your checks and the level of documentation depending on the client. Here’s a typical breakdown of clients based on their risk profiles:

- Low-risk clients: These are individuals with simple financial affairs and local connections. Basic screening and standard documentation are usually sufficient.

- Medium-risk clients: These may involve more complexity due to foreign connections or higher-value transactions. In this case, additional verification and occasional deeper checks may be appropriate.

- High-risk clients: This group includes PEPs, clients with complex ownership structures, or those linked to higher-risk jurisdictions. These cases require enhanced due diligence, more detailed documentation, and ongoing monitoring.

The important point is that the level of effort should match the level of risk: over-screening low-risk clients wastes time, while under-screening high-risk clients creates exposure.

Setting up your AML screening process

The only way to build a workable AML system is to clearly define your procedures, help your team understand it, and apply it consistently. Start by defining your firm’s approach, as it becomes the foundation of your internal policy:

- When screening happens: Screening takes place at onboarding, but it shouldn’t stop there. Most firms also include periodic reviews and trigger-based checks, such as changes in ownership or unusual client activity.

- How checks are performed: Manual processes may work at a very small scale, but they quickly become inconsistent and time-consuming. Most accounting firms move toward automated screening to ensure consistency and reduce admin.

- Who owns the process: Equally important is making sure your team understands their role in the workflow, including who’s responsible for reviewing results, when something should be escalated, and what constitutes a red flag.

- Documenting the outcome: Documentation ties everything together. You need a record of what checks were performed, what the results were, and how any matches or concerns were resolved. Even a “no match” result must be recorded.

This doesn’t have to be the exact process, but it can be a good starting point for your accounting firm.

What information you need from clients

AML screening is only as reliable as the data behind it. The items below are the minimum required for basic screening checks, but most firms will need a lot more information:

- Full legal name

- Date of birth

- Residential address

- Identification documents

For business clients, this extends further to beneficial ownership details. For higher-risk clients, you may also need information on source of funds and other supporting context. This is where many firms encounter friction because clients provide partial information and documents end up missing. It slows down screening while introducing unnecessary risk.

How Content Snare fits into your AML screening workflow

In most firms, AML screening becomes difficult not because the checks themselves are complex, but because the information needed to run them is scattered or incomplete. Content Snare addresses this by bringing information collection and screening into the same workflow.

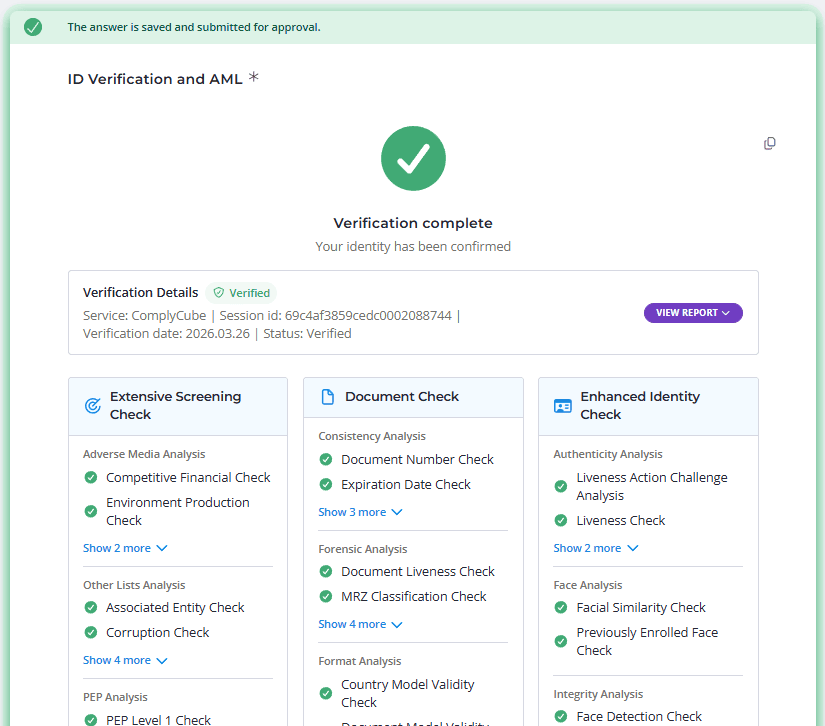

The platform helps you collect client details through structured requests, so you know the data is consistent and complete. Once that information is submitted, Content Snare can run PEP, sanctions, adverse media, and many other AML screening checks automatically - including checks for corruption and associated entities - without you having to move between tools or re-enter data:

The results are stored alongside the client’s information, along with any notes or decisions made during the review. This creates a centralized record of the entire process, which means you don’t have to manage external spreadsheets or third-party screening tools. When the workflow is structured this way, AML screening stops being a separate task. It becomes part of how your firm naturally collects, reviews, and manages client information.

If you want to see how this works in practice, you can explore the platform on the Content Snare tour page.

Screening doesn’t stop at onboarding

Though typically related to client onboarding, AML screening isn’t a one-time event. That’s because your clients’ circumstances evolve over time, while regulators continuously update sanctions lists. A practical approach to ongoing monitoring usually includes:

- Periodic re-screening of clients

- Reviews triggered by changes in client circumstances

- Annual reviews for higher-risk clients

That’s how you make sure that your screening remains accurate and up to date.

Pro tip: Beware of common AML screening mistakes

Even firms that take AML seriously tend to run into the same issues that reveal minor gaps in how the process is applied in day-to-day work:

- Treating screening as a one-off onboarding task

- Not screening beneficial owners or related parties

- Failing to document “no match” results

- Relying on manual processes that don’t scale

- Letting compliance become a box-ticking exercise

Over time, those gaps can undermine an otherwise solid AML screening. For this reason, it’s best to approach it as an ongoing risk assessment, supported by a clear and repeatable workflow.

Go beyond AML screening with Content Snare

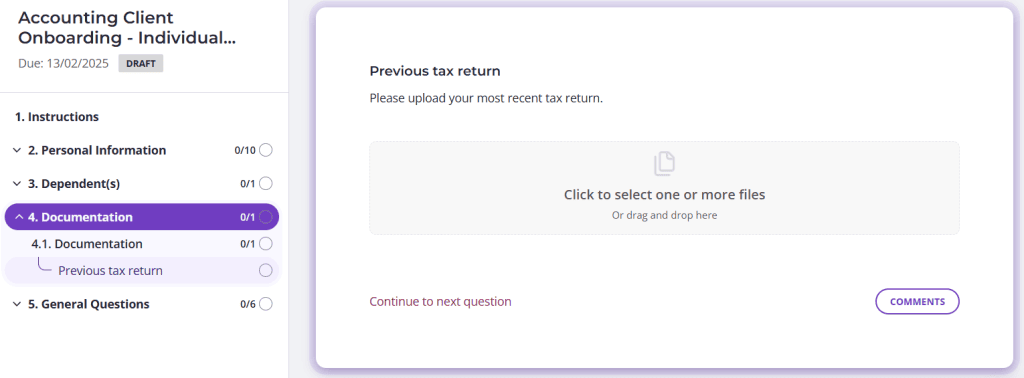

AML screening is only one part of a much larger challenge: getting accurate and complete information from clients in the first place. That’s where processes tend to break down most frequently. Content Snare is designed to solve that problem at the source.

Instead of treating AML as a separate task, our platform brings it into a structured workflow for collecting and managing client information. You send a request, your client is guided through exactly what they need to provide, and everything is automatically saved as they go:

From there, Content Snare supports the rest of your process with features like automatic reminders and in-app communication, so you’re not constantly following up or switching between tools. This is also why firms using our software spend 71% less time gathering information from clients.

To make things easier to get started, Content Snare includes dozens of templates built specifically for accounting and bookkeeping workflows. These are fully editable, so you can adapt them to your firm’s processes without starting from scratch. The platform is also ISO 27001 certified, following the strictest security standards to protect your clients’ data.

If you’d like to see how Content Snare works in practice, sign up for a 14-day free trial and explore the full workflow firsthand.